.png)

That creates a tough reality for independent 3PLs. Customers increasingly expect enterprise-grade capabilities, but SMB 3PLs do not have enterprise-grade capital budgets. The market’s response has been consolidation.

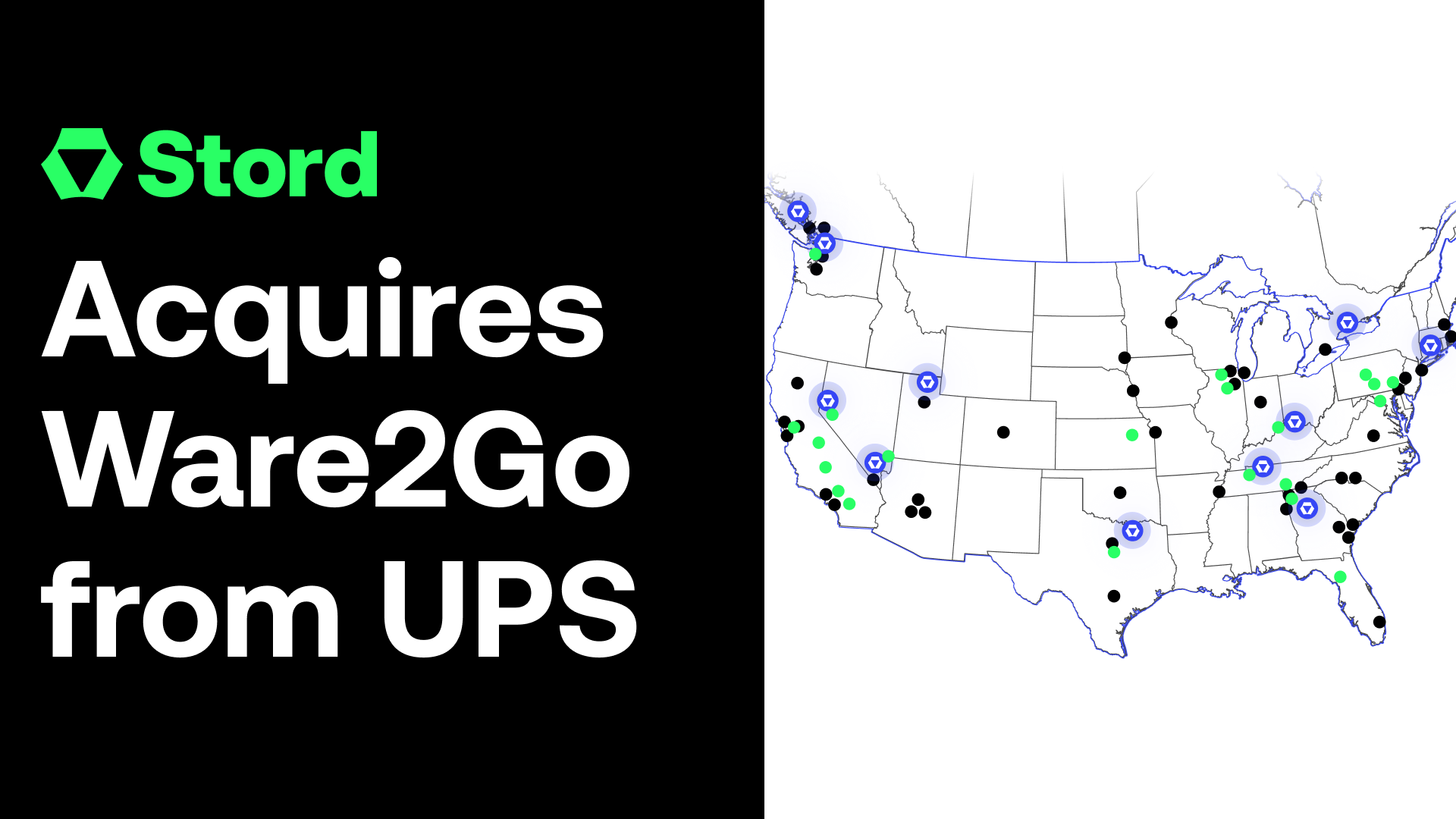

This past year, we have seen a spike of acquisitions across 3PL fulfillment, Shipfusion acquired Boxtrot to bring a boutique ecommerce fulfillment provider into a larger North American network. Stord acquired Ware2Go from UPS, then acquired Shipwire from CEVA Logistics to expand its global ecommerce fulfillment footprint. Larger platforms are buying density, customers, geographic coverage, and operational capabilities.

Logistics is a scale game, and that scale advantage is getting more obvious. The U.S. 3PL market rebounded in 2024 to about $308 billion in gross revenue, but for many smaller operators they're still struggling to compete with the larger players.

The message to SMB 3PLs is pretty clear: get bigger, or get bought. More scale can mean better facility utilization, stronger buying power, more capital access, broader geographic coverage, and more room to invest in automation and technology. But consolidation comes with real tradeoffs. Founders lose independence, local expertise, and customer relationships become less personal. A 3PL that used to customize kitting around each client becomes less flexible as it standardizes processes across a larger network. That standardization is necessary for scale, but it can also weaken the thing that made the business valuable in the first place.

Consolidation also does not solve the automation problem. Rolling up a group of SMB 3PLs may create more density and make it easier to invest in automation. Because the facilities were designed around people, it’s a tall order to spend tens or hundreds of millions of dollars on ASRS, massive conveyor networks, custom sortation systems, and highly engineered greenfield facilities.

Traditional automation has always favored the biggest players because it rewards companies with the most capital, the most volume, and the most predictable workflows. It is expensive, fixed, and difficult to justify unless you have enough throughput to amortize the investment. It works best when demand is stable, SKUs are predictable, and the building itself can be designed around the system.

That is not the reality for most SMB 3PLs. They operate in the messy middle of logistics: changing customer profiles, seasonal spikes, custom kitting, variable SKUs, returns, late inbound freight, special projects, and exceptions that do not fit neatly into a rigid automation model. That messiness is often the reason customers choose them in the first place!

This is why general purpose robots matter. The first automation wave that can truly help SMB 3PLs is a giant fixed system built into the warehouse. It is a flexible robotic labor that can be dropped into existing facilities, moved between workflows, and deployed without rebuilding the entire operation.

General purpose robots change the automation equation because they are mobile, flexible, and task-adaptable. They can work inside human-designed warehouses. They can be assigned to different tasks. They can be deployed incrementally instead of requiring a massive upfront transformation.

There is another lesser known part of this shift: general purpose robots do not just automate labor. Enterprise logistics companies have spent years and millions of dollars building systems for inventory visibility, facility mapping, security monitoring, workflow analytics, exception detection, and real-time operational reporting. For SMB 3PLs, those capabilities have often been out of reach.

General purpose robots can change that because they are already moving through the facility, seeing the environment, interacting with inventory, and touching core workflows. A robot that is picking bins, decanting inventory, polybagging items, or moving through aisles is also collecting data about where inventory is, how goods flow through the building, which areas are congested, which SKUs create exceptions, and how the physical layout actually performs. The robot becomes both labor and a source of data.

This matters because labor is one of the biggest cost centers in a 3PL operation. When a 3PL is fighting labor availability, overtime, training churn, and margin pressure, it has less energy to focus on what actually differentiates the business. Flexible robotic labor can give the business back time, margin, and management attention.

SMB 3PLs should be doubling down on the things enterprise 3PLs are less suited for. Robots do not replace that part of the business, but rather protect it by taking on repetitive, physically demanding work.

The timing matters because through Amazon’s new Supply Chain Services, they are increasingly turning their internal logistics stack into an external service for other businesses. Amazon has built one of the most automated logistics networks in the world. Its warehouse robot fleet has passed one million robots and they spend hundreds of billions each year on R&D.

That should get everyone’s attention, not just SMB 3PLs. Companies like DSV, DHL, Kuehne+Nagel, GXO, and others have massive scale and serious automation programs, but can't compete with efficiency gains of purpose built automation. Amazon has been compounding advantages across software, robotics, fulfillment density, marketplace demand, last-mile delivery, cloud infrastructure, and AI for years.

Traditional automation increased the advantage of scale, but general purpose robotics may be the first automation wave that reduces it. A fixed automation system rewards the company with the largest facility, the most capital, and the most predictable volume. General purpose robots reward the company that works within human-centric environments, knows where labor is being wasted, and can deploy flexible capacity where it matters most.

For SMB 3PLs, that is a unique opportunity. They do not need to become enterprise 3PLs to survive. They do not need to sell to the largest platform in the market. They need automation that fits their buildings, their customer mix, and their operating reality. They need systems that can be deployed inside existing facilities, not only inside new greenfield mega-warehouses.

The future of SMB 3PLs will not be won by copying Amazon. It will be won by combining what independent 3PLs already do best with automation that finally fits their world: trusted relationships, custom service, local specialization, and flexible robotic throughput.

At Yondu, we are building for that future. Our automated mobile bin-picking, polybagging, and decanting robotics solutions are designed to deploy inside existing facilities and automate real warehouse workflows without requiring SMB 3PLs to rebuild their operations from the ground up.

The goal is simple: give independent 3PLs access to flexible robotic labor, so they can compete on cost without giving up what makes them different.

SMB 3PLs do not need to become giants to thrive. They need the right robots.